Mortgage Surveyors Valuation: Lender vs. Surveyor 2026

You've got your mortgage offer. You scan the paperwork, spot a valuation fee, and assume that means someone's checked the place properly.

That's where buyers get caught out.

A lender's valuation is about the bank's risk, not your risk. It tells the lender whether the property is suitable security for the loan. It does not tell you if the Victorian terrace in Lewisham has damp behind the panelling, if the warehouse conversion in Bermondsey has movement cracks hidden by fresh paint, or if the loft conversion in a Bromley semi looks tidy but was done badly.

Plenty of buyers only realise this after completion, when the first repair bill lands.

Table of Contents

- Your Mortgage Offer Has Arrived What Is This Valuation Fee

- The Lender's Mortgage Valuation Unpacked

- What a Proper RICS Surveyor's Report Gives You

- Mortgage Valuation vs RICS Survey A Direct Comparison

- Process Costs and Timescales for a Survey in London

- Common Pitfalls Why a Valuation Is Never Enough

- Making a Confident Decision on Your Property

- Frequently Asked Questions

Your Mortgage Offer Has Arrived What Is This Valuation Fee

This usually starts the same way. You've had an offer accepted, the estate agent is pushing for speed, the solicitor has sent a few forms, and the lender's paperwork mentions a valuation. You think, good, someone's checking the place.

That assumption is the problem.

A mortgage surveyors valuation sounds as if it protects you. It doesn't. It protects the lender. If the bank is lending against a flat in Greenwich or a terrace in Peckham, it wants to know whether the property stacks up as security for the mortgage. That's the job.

It isn't there to advise you on repairs. It isn't there to tell you what needs urgent attention. It isn't there to stop you buying a money pit.

Practical rule: if the report is commissioned for the lender, the lender is the client. You are not.

This is why buyers feel blindsided. They see “valuation”, they pay a fee, and they assume they're getting a survey. Then they move into a flat conversion in Camberwell and discover damp staining was painted over, the roof has had patch repairs for years, and the chimney breast removal downstairs was never properly assessed.

The wording matters. A valuation and a survey are not the same thing. Treating them as if they are is how costly mistakes happen.

The Lender's Mortgage Valuation Unpacked

What the lender is paying for

You buy a Victorian terrace in Walthamstow. The lender signs it off. Weeks later, you find long-standing movement masked by fresh plaster, rotten sash window frames, and a patched rear addition with no proper ventilation. That is how buyers get caught. The valuation did its job for the bank. It did nothing for you.

A lender's mortgage valuation is a lending decision tool. The surveyor, or the lender's system, is checking whether the property is suitable security for the loan and whether the figure broadly supports the amount being borrowed.

That is a narrow brief.

The valuer is looking for issues that could affect marketability or sale price in a serious way. Severe movement. Clear damp. Non-standard construction. Short lease problems. Unusual layout. Major legal or physical defects that make the asset harder to sell if the lender ever has to recover its money.

That still falls miles short of a proper buyer's survey, especially in London.

London stock is messy. Victorian terraces have hidden defects from piecemeal alterations, bridged damp courses, tired roofs and chimney breast removals. Warehouse conversions can carry fire separation concerns, awkward insulation details, complicated service charges and commercial-style construction that lenders and buyers both need to understand properly. A brief valuation, particularly a remote one, will not give you the level of scrutiny those properties often need.

Why the "free valuation" line misleads buyers

Estate agents and mortgage paperwork often make the valuation sound like a useful freebie. It isn't a free survey. It is a basic risk check wrapped into the lending process.

In many cases, there may not even be a full internal inspection. Lenders now use automated valuation models, desktop assessments and limited inspections for plenty of mainstream properties, as explained in the HomeOwners Alliance guide on mortgage valuations. That suits the lender because it keeps cost and turnaround under control.

For a buyer, that shortcut creates a blind spot.

A computer model can compare sales evidence. It cannot smell damp in a lower ground floor flat in Fulham. It cannot judge the quality of a loft conversion in a Hackney terrace from old listing photos. It cannot tell you whether cracking around a warehouse conversion window opening is cosmetic or a sign of movement.

That is the gap buyers need to understand. Automated lender checks are about lending risk. A RICS survey is about building risk.

If you want the selling-side perspective as well, this guide for sellers on valuations is worth reading. It helps show why valuation evidence and buyer protection are two separate things.

For extra context on how pricing evidence is judged across the capital, see this explanation of house valuation in London.

The lender wants enough comfort to release funds. You need enough evidence to avoid buying a problem.

What a Proper RICS Surveyor's Report Gives You

A proper RICS survey is about your decision, your advantage and your risk. It's the difference between buying with open eyes and hoping for the best.

An independent surveyor inspects the property for defects that matter to a buyer. That means visible signs of damp, timber decay, roof spread, movement cracks, poor alterations, failed windows, defective rainwater goods, unsafe detailing and all the other things that cause grief after completion.

Level 2 suits many flats and modern homes

The RICS Home Survey Level 2 is designed for conventional properties built after 1890 and uses a clear traffic light system. Condition Rating 3 means defects are serious and need repair, replacement, or urgent investigation, as explained in Legal & General's overview of the Level 2 survey.

That traffic light format is useful because buyers can read it quickly. Green means less concern. Amber means attention needed. Red means stop, understand the issue, and price the risk properly.

For a modern flat in Canary Wharf, a standard purpose-built flat in Blackheath, or a conventional 1930s house in Sidcup that appears in reasonable condition, Level 2 is often the sensible starting point.

Level 3 is the right call for older and altered property

A Level 3 Building Survey is the right choice when the building is older, more altered, non-standard or plainly tired. That includes a Victorian terrace in Lewisham, an Edwardian house in Dulwich, a flat conversion in Brockley, or a warehouse conversion in Bermondsey where structure, services and past works can all raise awkward questions.

A Level 3 goes further. It gives you a fuller picture of the construction, visible defects, likely causes and what needs further investigation.

Use this simple rule of thumb:

- Choose Level 2 for a conventional property in apparently reasonable condition.

- Choose Level 3 for older homes, heavily altered homes, listed buildings, non-standard construction and anything that already worries you.

- Choose caution if the estate agent says “it's just cosmetic”. That phrase covers a lot of sins.

If you want a straightforward explanation of survey types and how RICS reporting works, this article on what a RICS survey is sets it out clearly.

Buy the survey that matches the building, not the one that feels cheapest on the day.

A proper survey report also gives you something a lender's valuation doesn't. It gives you grounds to renegotiate. If the surveyor identifies roof defects, defective pointing, damp ingress around a rear addition, or signs of movement around openings, you've got evidence. That can change the conversation before exchange.

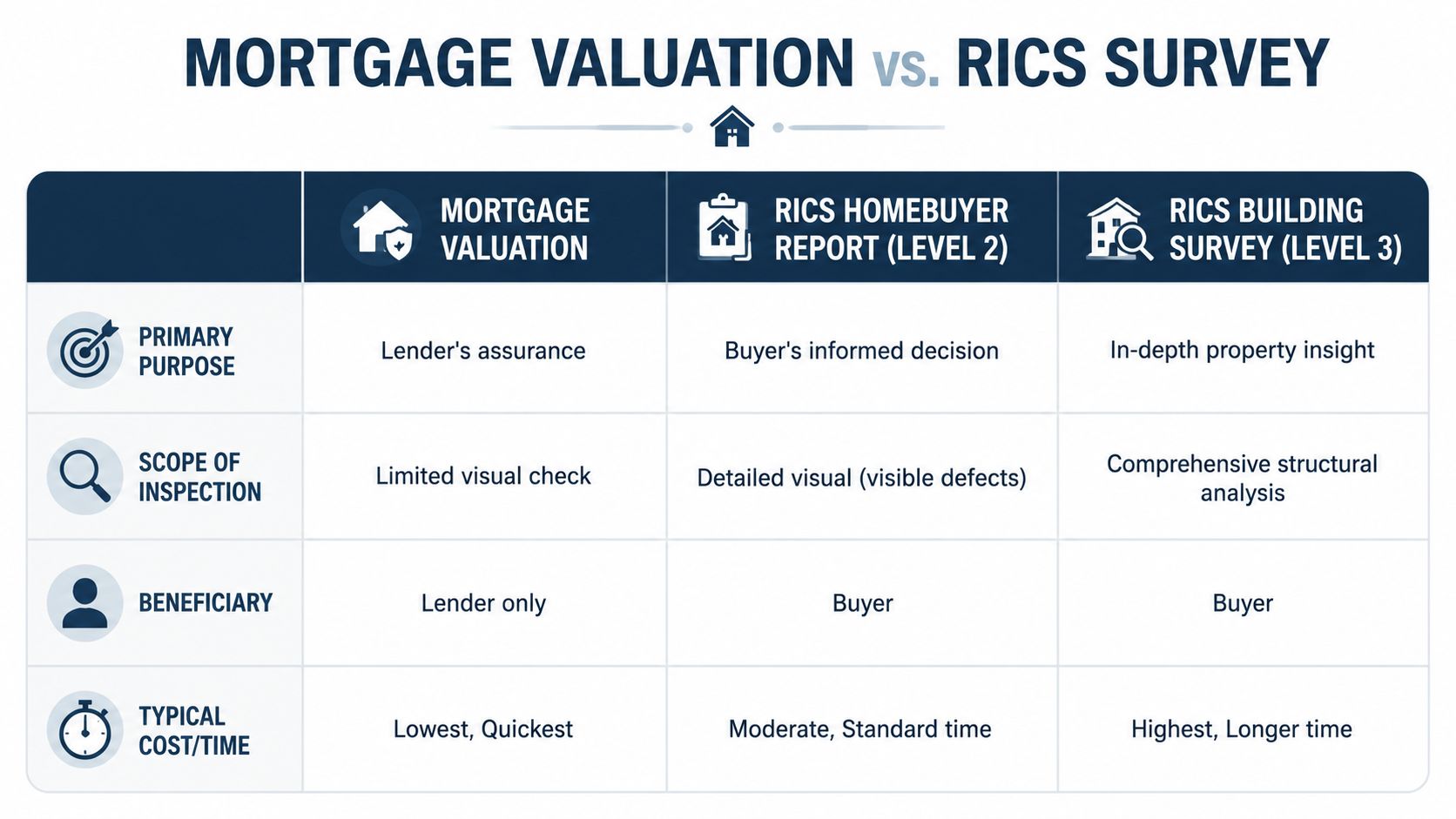

Mortgage Valuation vs RICS Survey A Direct Comparison

A lot of confusion clears up once you put the services side by side.

A mortgage valuation is a visual observation only, not a detailed condition assessment, and its primary purpose is to confirm the property is suitable security for the loan. It does not explain causes, costs or the extent of problems, as stated in this video explanation of mortgage valuations.

Valuation vs Survey At a Glance

| Feature | Mortgage Valuation | RICS Home Survey Level 2 | RICS Building Survey Level 3 |

|---|---|---|---|

| Primary purpose | Lender's assurance | Buyer's informed decision | Buyer's in-depth understanding |

| Who it serves | Lender | Buyer | Buyer |

| Inspection scope | Limited visual check or remote assessment | Detailed visual inspection of visible defects | More detailed inspection of structure and condition |

| Report detail | Minimal | Clear condition ratings and practical advice | Broader technical detail on defects and risks |

| Repair guidance | No meaningful buyer advice | Yes, in practical terms | Yes, with fuller discussion |

| Best suited to | Mortgage underwriting | Conventional homes in reasonable condition | Older, altered or non-standard property |

| Useful for renegotiation | Rarely | Often | Strongly, where defects are found |

Here's the blunt version.

If you're buying a neat-looking maisonette in Clapham, the lender may be content with a light-touch valuation. If you're the one paying for the roof leak, decayed sash boxes or defective flat roof covering later, the lender's comfort doesn't help you.

The bank can be satisfied and you can still inherit a long list of repairs.

That's why “mortgage surveyors valuation” is a phrase people search, but it's also where people mix up two different products. One is a lending check. The other is buyer protection.

Process Costs and Timescales for a Survey in London

Your mortgage offer lands, the estate agent starts pushing for progress, and everyone acts as if the hard part is done. It isn't. In London, this is the point where buyers make expensive mistakes by treating the lender's valuation as if it were proper due diligence.

Book your survey as soon as the memorandum of sale is agreed. That gives you time to find out whether the “charming” Victorian terrace has movement, hidden damp, failed roof coverings or alterations done on the cheap. It also matters for warehouse conversions and other non-standard flats, where access, leasehold paperwork and odd construction details can slow everything down.

How the process usually runs

Start with the surveyor, not the lender.

A good firm will want the address, asking price, property type, age, tenure and any concerns already raised by the agent or seller. From there, the job is to pick the right level of inspection. A modern flat in Woolwich may suit a Level 2. A heavily altered terrace in New Cross, a period conversion in Hackney, or an old warehouse flat with exposed steel and flat roofing usually calls for a Level 3.

Then comes access. In London, that is often the part that holds things up. Mansion blocks in Westminster can have awkward booking systems. Docklands developments may need concierge approval. Probate sales can drift because keys are with relatives, not occupants.

Once access is confirmed, the inspection is booked and the report follows after the visit. Read it before exchange. That sounds obvious, but plenty of buyers leave themselves no room to renegotiate or walk away.

What you pay for

The gap in price reflects the gap in protection.

A mortgage valuation is usually the cheaper item, and some lenders roll it into the mortgage package and call it free. Ignore the label. It is still the lender's check, not your advice. A proper RICS survey costs more because the surveyor is spending time inspecting the property, identifying defects, assessing risk and writing a report you can use.

Price depends on the property, not just the postcode. Older buildings need more attention. So do homes with extensions, roof alterations, converted lofts, flat roofs, signs of movement or non-standard construction. Larger homes take longer. Complicated leasehold blocks take longer too.

That is why the cheapest quote is often the wrong one. If a surveyor is inspecting a tired conversion in Peckham or a Victorian house in Sydenham for a bargain fee, ask yourself how much time they can really spend on it.

A sensible guide is to budget by risk, not by wishful thinking:

- Modern, conventional flats: usually simpler and quicker, if the block is straightforward

- Victorian and Edwardian houses: higher risk, more defects, more reporting detail

- Warehouse conversions and unusual buildings: slower to assess and more likely to need a deeper look

- Large or heavily altered properties: more inspection time and a fuller report

If you want a clearer breakdown of the difference between lender charges and buyer survey fees, this guide on how much a house valuation costs is useful.

Timescales in the real world

Straightforward instructions can move quickly. London purchases are rarely straightforward.

A survey can often be booked within days if access is easy and the property is conventional. Reports then follow after inspection, depending on the survey type and the surveyor's workload. But delays are common where sellers are juggling tenants, managing agents are slow, or the building itself is awkward to inspect.

My advice is simple. Instruct early, chase access hard, and leave space in the transaction for the report to be read properly. The survey is not a box to tick. It is your chance to spot trouble before the legal commitment is made.

Common Pitfalls Why a Valuation Is Never Enough

The biggest mistake is simple. Buyers think the lender has “checked it”.

No. The lender has checked enough for the lender.

Over 1.2 million UK mortgage valuations in 2024 were conducted without physical inspection, yet 18% of buyers later discovered undetected defects within 12 months of purchase, a risk noted as especially acute in London's older housing stock. That matters in this city because so much of the stock is layered with age, conversion work and patch repairs.

The free valuation myth

The words “free valuation” fool people. They sound generous. They sound as if the lender is covering something useful for you.

They're not.

A free valuation means the lender has chosen not to charge you separately for its own risk check. It does not mean you've been given a Level 2 survey. It does not mean anyone is advising you on hidden defects. It does not mean the property is sound.

That misunderstanding is common because the paperwork is easy to skim and the transaction moves fast. Buyers in places like Stratford, Walthamstow and Battersea often feel pressure to keep things moving. Skipping an independent survey to save money can be a very expensive decision.

London stock hides problems well

London property can look fine and still be troublesome.

A Victorian terrace in Catford may have suspended timber floors with poor ventilation and decay risk. A period flat in Southwark may have historic movement around bay windows. A converted warehouse in Bermondsey may have awkward thermal bridging, roof issues, water ingress around parapets, or unauthorised changes hidden behind smart finishes.

Watch for these common traps:

- Fresh decoration: paint can hide damp staining and crack repairs.

- Loft conversions: neat plasterboard doesn't prove the structure or fire separation is right.

- Basement areas: lower ground accommodation can conceal moisture issues for years.

- Flat conversions: sound insulation, structure and shared maintenance are often weaker than buyers assume.

If a property has age, alterations or a complicated history, relying on a valuation alone is asking for trouble.

There's another practical point. If the lender down-values the property, buyers often panic because the mortgage offer changes. An independent survey won't stop a down-valuation, but it can give you evidence on condition and defects when you need to renegotiate sensibly rather than argue blind.

Making a Confident Decision on Your Property

The position is straightforward. A lender's valuation protects the lender. A survey protects you.

If you're buying in London, that distinction matters even more because the housing stock is so mixed. A shiny flat in a converted block, a worn Victorian terrace, a 1930s semi with later extensions, they all carry different risks. The lender only needs enough comfort to lend. You need enough information to live with the building and pay for its defects.

A proper independent RICS survey is money spent before the mistake, not after it. That's the sensible way to look at it.

If the purchase also has tax, ownership structure or rental planning issues around it, specialist advice matters there too. For that side of the picture, this guide to choosing UK property accountants is a useful starting point.

Corinthian Surveyors London LTD is an independent firm of RICS Chartered Surveyors and Valuers based in Forest Hill, with CABE-qualified expertise and no ties to lenders, estate agents or developers. If you want straight advice on the right survey for the property you're buying, call 0800 00 16 422 before you exchange, not after.

Frequently Asked Questions

Is a mortgage valuation the same as a survey

No. A mortgage valuation is for the lender's lending decision. A survey is for your understanding of the property's condition.

Can a desktop valuation spot damp or structural problems

Not reliably. Remote valuation is about lending risk and broad value, not a detailed inspection of hidden or developing defects.

Should I get a Level 2 or Level 3 survey in London

For a conventional property in reasonable condition, Level 2 is often suitable. For older, altered, non-standard or obviously tired property, Level 3 is the safer choice.

Are mortgage valuations regulated

Yes. The RICS Valuation, Professional Standards, known as the Red Book, governs bank lending valuations and was updated effective 1 January 2026, ensuring they are legally defensible and consistent, as outlined in Nuvén Surveyors' explanation of RICS valuations.

If you need an independent view before you commit, Corinthian Surveyors London LTD provides residential surveys and valuations across London, the Home Counties and the South of England. Clive Thompson is RICS and CABE qualified, the firm is regulated by RICS, registered under the RICS Valuers Registration Scheme and insured by Royal Sun Alliance. That matters because independence, local knowledge and proper professional standards are exactly what buyers need when a lender's valuation isn't enough.