House Valuation London: Your 2026 Guide to RICS & More

You're probably in one of these positions right now. You've had an estate agent give you a cheerful figure for your flat in Islington, your solicitor has asked for a probate valuation on a house in Lewisham, or your mortgage lender has come back with a number that's lower than the price you agreed.

That's where people get caught out. They assume every “valuation” is the same thing. It isn't. In London especially, the gap between an optimistic market appraisal and a proper valuation can decide whether a sale holds together, whether a mortgage goes through and whether a tax submission stands up to scrutiny.

If you want a reliable house valuation London figure, you need to know who the valuation is for, what standard it has to meet and what evidence sits behind it. That's the difference between a loose opinion and a defensible number.

Table of Contents

- What Is a House Valuation and Why You Need a Real One

- The Different Types of House Valuation Explained

- How a London Property Valuation Is Actually Conducted

- Key Factors That Drive Property Value in London

- Common Pitfalls and Understanding Down Valuations

- Choosing a Surveyor and Preparing Your Property

- FAQ

What Is a House Valuation and Why You Need a Real One

If you're dealing with probate on a terraced house in Catford or getting ready to sell a flat in Hackney, the first number you hear is often the wrong one to rely on.

An estate agent's market appraisal is usually a pricing opinion. It helps them pitch for the instruction. A RICS market valuation is different. It's evidence-led, written by a regulated professional and capable of being used for legal, tax and lending purposes where the brief requires that standard.

That distinction matters more in London because the market is uneven. In February 2026, London house prices fell by an annual rate of 3.3% to an average of £542,304, and the wealthiest boroughs saw steeper falls, with Kensington and Chelsea dropping 8.4% from £1,390,000 in April 2025 to £1,273,000 in April 2026, according to the Financial Times reporting on London housing data. In that sort of market, a hopeful asking figure and a supportable valuation can be miles apart.

Why the right valuation matters

A proper valuation isn't just for selling. You may need one for:

- Probate so the value reported for inheritance tax is properly evidenced

- Divorce or separation where solicitors need a neutral figure

- Capital gains tax where retrospective dating may be required

- Mortgage lending where the bank wants to know the security value, not your opinion of the place

- Price negotiations where defects, alterations or local comparables need to be reflected

Practical rule: if the figure has to stand up with a lender, HMRC, a solicitor or the court, an estate agent's appraisal isn't enough.

There's a place for presentation as well. If you're selling, things like tidying, repairs and even digital property enhancements can help buyers see the property properly. But presentation doesn't replace valuation evidence. A polished listing may attract viewings. It won't persuade a lender's valuer to ignore poor comparables, cladding risk or structural defects.

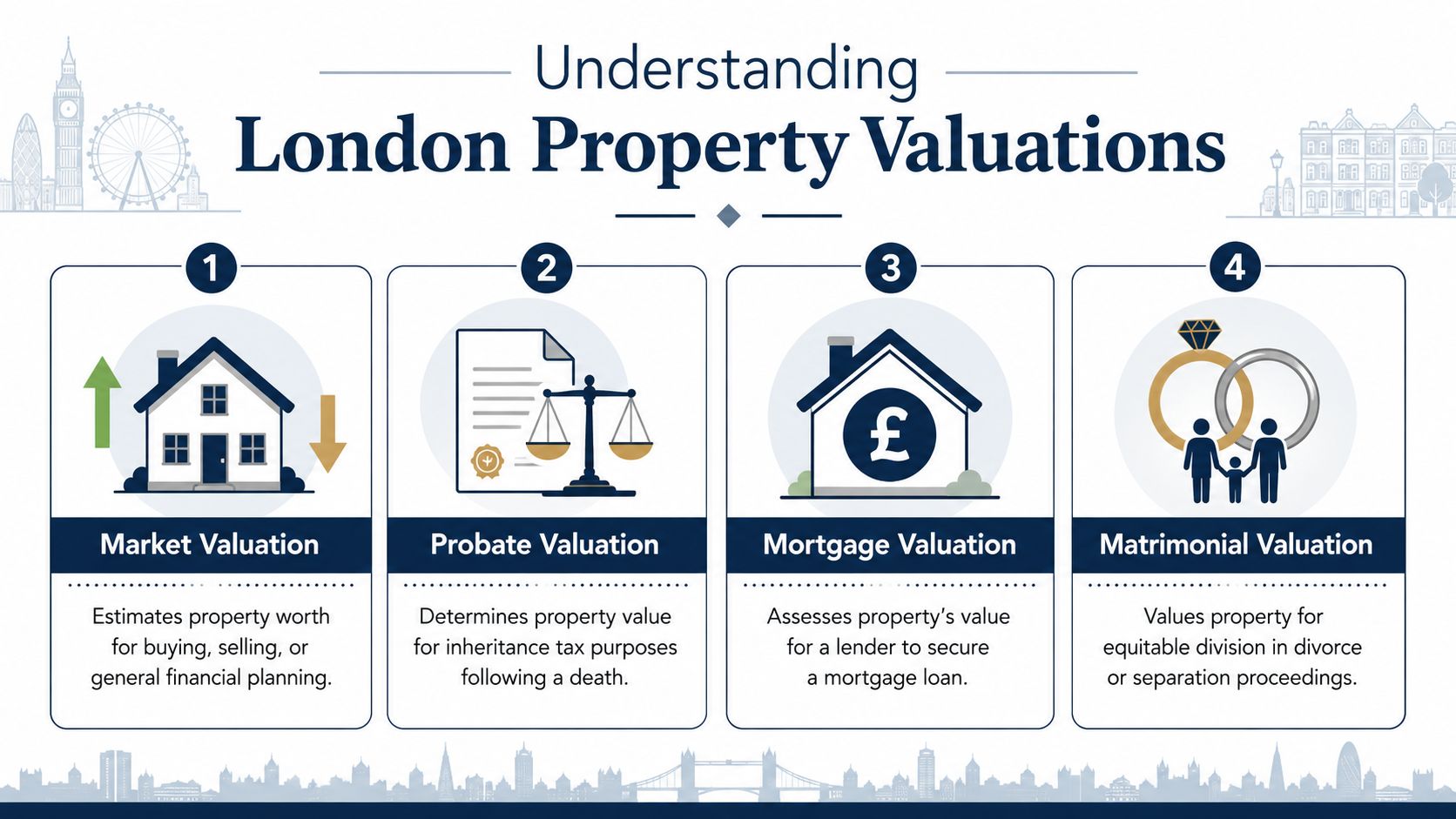

The Different Types of House Valuation Explained

People use the word valuation as if it means one report. It doesn't. The type you need depends entirely on the job the report has to do.

A useful starting point is this: if you're unsure what survey and valuation product sits where, this guide on what a RICS survey is helps separate condition reports from valuation work.

Market valuation

This is the report people usually need when they want to know what a property should sell for on the open market.

The valuer looks at the property itself, its condition, its location and recent comparable sales. They adjust for size, layout, outlook, tenure, defects, extensions and overall presentation. In London, that means a Victorian terrace in Brockley won't be treated like a 1930s semi in Bromley or a warehouse conversion in Bermondsey just because the floor area looks similar.

A market valuation is the sensible option when you want to set a realistic asking price, test an estate agent's figure or negotiate a purchase.

Mortgage valuation

This one causes endless confusion. A mortgage valuation is for the lender, not for you.

The bank wants to know whether the property is adequate security for the loan. It is not a substitute for a survey. It may be brief. It may not investigate the building in the depth a buyer assumes. If there's damp behind furniture, movement in the rear addition or poor-quality alterations in the loft, a mortgage valuation is not there to protect you from that risk.

A lender's valuation answers one question. Is this acceptable security for the loan amount. It does not answer the question buyers actually care about, which is what they're taking on.

Probate and tax valuations

Probate valuations are used after a death to establish the value of the property at the relevant date. Capital gains tax work may require a retrospective valuation based on the market at an earlier point in time.

These are not “best guess” jobs. The figure needs to be reasoned and documented. For probate in places like Dulwich, Blackheath or Kensington, small differences in specification, condition and exact location can alter value materially, so sloppy desktop-only assumptions are risky.

Matrimonial valuation

When a property forms part of a divorce or separation, the valuation must be neutral and properly evidenced.

This is not the time for a selling price fantasy. Solicitors and the court need an independent opinion, not a sales pitch. The report has to be balanced, transparent and capable of scrutiny.

A quick comparison

| Valuation type | Mainly for | Main purpose | What to watch |

|---|---|---|---|

| Market valuation | Owner, buyer, seller | Sale, purchase, planning | Needs proper comparables and condition assessment |

| Mortgage valuation | Lender | Loan security | Not a survey for the buyer |

| Probate valuation | Executor, solicitor, HMRC context | Inheritance tax and estate administration | Must reflect the correct valuation date |

| Matrimonial valuation | Solicitors, separating parties | Asset division | Independence is essential |

One more point. Don't confuse valuation cost with survey cost. They're different instructions. The average cost of a RICS HomeBuyer Report (Level 2) in London ranges from £450 to £750, with larger homes in central boroughs such as Kensington or Chelsea reaching up to £900, according to Harding Surveyors on London HomeBuyer Report costs. That figure relates to a survey product, not every valuation brief, but it gives you a rough sense that proper professional advice isn't free and shouldn't be treated like a tick-box.

How a London Property Valuation Is Actually Conducted

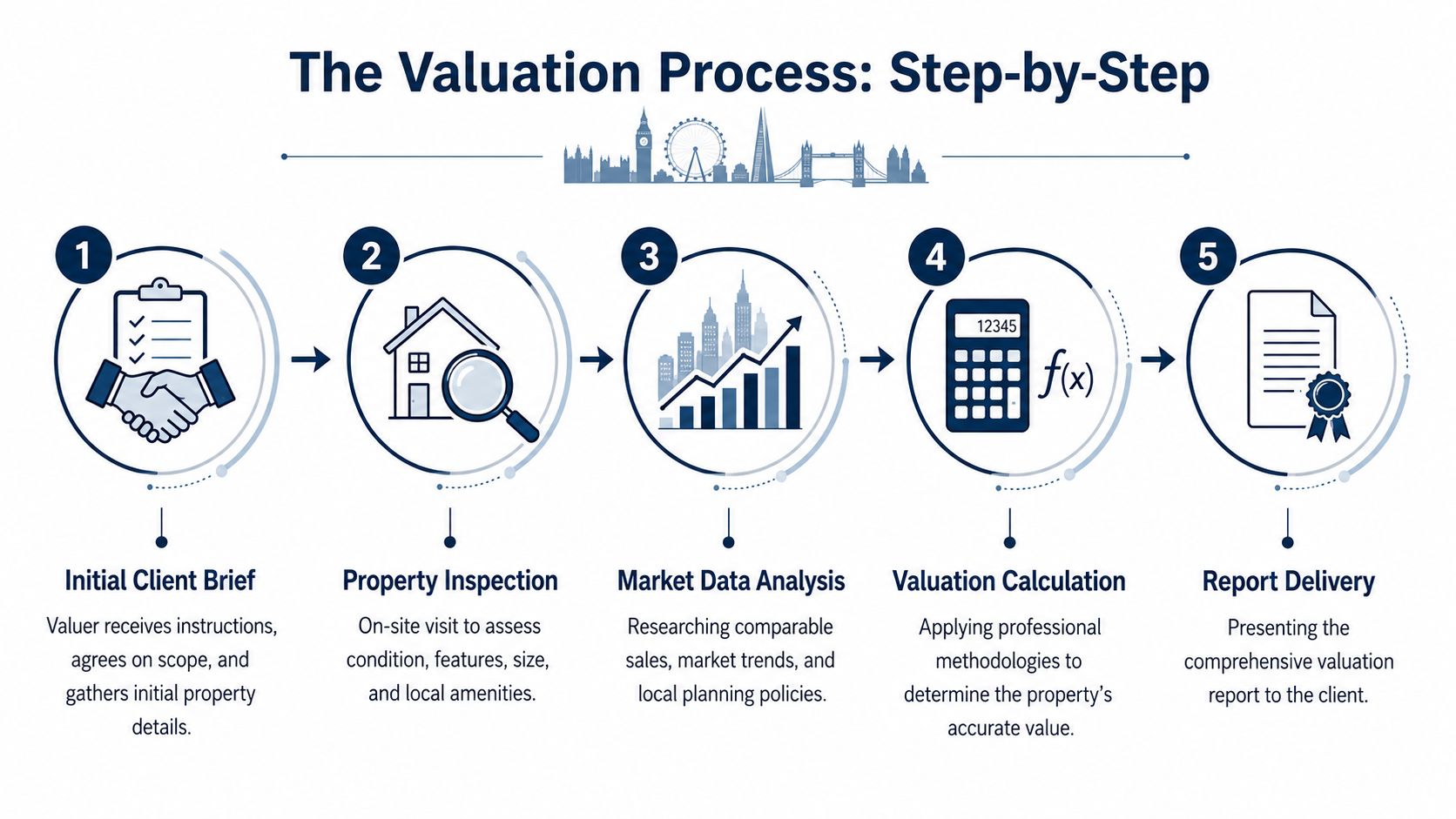

A decent valuation is method, not theatre. If someone gives you a figure in five minutes without proper inspection and evidence, treat it with caution.

The inspection on site

First comes the property itself. The valuer inspects the accommodation, measures and notes the layout, and looks at condition, repair, quality of finish and anything unusual that affects value.

That includes obvious defects and less obvious ones. Damp staining, roof spread, poor-quality flat roof coverings, movement cracks, timber decay, non-standard construction, a missing wall in a badly altered reception room, an unapproved rear extension, a loft conversion with no paperwork. These things affect value because buyers and lenders react to them.

For London stock, local building type matters. A Victorian house in Forest Hill may carry issues with suspended timber floors, chimney breast alterations, ageing roof coverings and original plaster. A flat conversion in Camberwell may raise questions about sound insulation, fire separation, lease terms and who maintains the structure.

The desktop work that actually supports the figure

The inspection is only half the job. The figure has to be anchored to evidence.

A technically rigorous London valuation requires the valuer to combine property-specific structural characteristics with HM Land Registry sold price data, and postcode transaction history can be used to identify exact sale prices, dates and property types within a 1-mile radius, as explained in Property Solvers' discussion of HM Land Registry-led valuation practice. That is why automated tools often miss the mark. They can't judge the quality of a rear extension, the effect of damp or the difference between a tired ex-rental and a properly refurbished owner-occupied flat.

If you want a wider primer on site value and what sits beneath a property's worth, this piece on understanding land valuation is useful background. It won't replace a building inspection, but it does help explain why land, planning context and use all feed into value.

Later in the process, the report is put together with the evidence and reasoning set out clearly.

For practical examples of how valuation reports are structured, the article on property valuation reports is worth reading.

What online tools can't do

Online estimates are fine for idle curiosity. They are not reliable enough for decisions with consequences.

Here's what they usually miss:

- Condition: an algorithm can't smell damp or see hidden roof defects

- Alterations: it won't know if the loft conversion lacks approval

- Block issues: cladding, lease defects and service charge problems often sit outside the estimate

- Micro-location: one street in Walthamstow can outperform the next. One side of a road in Richmond can be noisier, less attractive or in a different school catchment

A proper house valuation London report joins all of that up. That's what you're paying for.

Key Factors That Drive Property Value in London

People love easy rules. Zone 2 beats Zone 4. Bigger beats smaller. Near a station beats far from a station. Real valuation work is more awkward than that.

In London, the same borough can contain very different sub-markets. Southwark has period terraces, ex-local authority flats, luxury riverside blocks and compromised stock near busy roads. One broad label tells you very little.

Condition, construction and defects

Condition moves value fast. Two houses in Sydenham with the same floor area can differ sharply if one has modern services, sound roofs and sensible alterations, while the other has penetrating damp, tired windows and movement to the rear addition.

Construction type matters as well. Older stock across Greenwich, Lewisham and Southwark often comes with quirks that generic online valuations gloss over:

- Victorian and Edwardian houses: look out for lath and plaster, original pipework, shallow sub-floor ventilation and chimney breast removals

- Flat conversions: poor sound insulation, unclear maintenance liabilities and awkward lease terms can hurt value

- Listed buildings and conservation area homes: special character can add appeal, but restrictions on works and repair methods can narrow the buyer pool

On site, I'm not asking whether the kitchen looks fashionable. I'm asking whether the building has defects, risk or legal baggage that a buyer or lender will price in.

Location still matters, but not in the lazy way people think

Location is not just postcode vanity. It's the exact setting.

A house in Dulwich with a conservation area setting and attractive street scene may perform very differently from a similar-sized house on a noisier road with awkward parking. In Stratford, transport links may support value. In Richmond or Blackheath, buyers often pay attention to catchments, outlook and overall character. In Bromley and Orpington, plot shape, parking and extension potential can become major pricing points.

A valuer also looks at what has sold nearby, not what sellers hope to achieve. As noted in the earlier section, London's market has not been moving evenly, so local evidence matters more than broad sentiment.

Features that now change value quickly

Some issues have become far more important in recent years.

In 2025, high-rise flats with unresolved EWS1 forms saw valuation reductions of up to 12–15% in Southwark and Tower Hamlets, and homes in flood zones 2–3 in parts of Lewisham and Bexley faced 5–8% valuation discounts, according to e.surv's notes on valuation issues including EWS1 and flood risk. That's not theory. It has a direct effect on sales, lending and negotiations.

Other factors also carry weight, even where the adjustment is more case-specific:

| Factor | Why it affects value | London example |

|---|---|---|

| Energy efficiency | Buyers increasingly notice running costs and upgrade burden | Older terraces in Peckham or Catford with poor thermal performance |

| Tenure and lease terms | Short leases and high charges reduce appeal | Flats in converted buildings across Islington or Lambeth |

| Flood exposure | Insurance and buyer caution can affect price | Thames-side or low-lying parts of Bexley and Lewisham |

| Cladding and fire documentation | Lenders may restrict or delay lending | Taller blocks in Southwark, Tower Hamlets and similar boroughs |

The lesson is simple. Value isn't created by square footage alone. It sits in the details, and London is full of details that change the number.

Common Pitfalls and Understanding Down Valuations

A down valuation is one of the most stressful parts of a transaction because it arrives late and causes immediate damage. The buyer has agreed a price, the seller has made plans and then the lender's figure lands below the deal.

What a down valuation actually means

It does not automatically mean the surveyor has got it wrong. It usually means the agreed price is ahead of the evidence the lender is prepared to rely on.

That gap has been a real issue in London. In 2025, 18% of London mortgage applications were delayed or rejected due to down valuations, according to HomeOwners Alliance on down valuations. This is especially painful for high loan-to-value buyers because they don't have spare cash to bridge the difference.

The most common causes are boring rather than dramatic:

- The agreed price was too ambitious

- Recent comparables don't support the deal

- The valuer has spotted condition issues

- The lender is cautious about the property type

- The market has softened between offer and valuation

What to do if it happens

Start with the evidence. Don't start with outrage.

If you're challenging a valuation, you need strong comparable sales. The best evidence is usually recent, genuinely similar stock in the immediate area. A broad borough average won't do the job. A larger, refurbished flat two roads away with a better lease won't do either.

Useful approach: build your challenge around recent sold comparables that are as close as possible in location, type and condition. If the evidence is weak, accept that quickly and renegotiate.

You then have four realistic options:

Renegotiate the price

This is usually the cleanest answer. If the valuation is evidence-based, the seller needs to confront the market rather than the buyer.Increase your deposit

If you have the funds, you can cover the gap yourself. Many buyers can't.Challenge the valuation

This only works if you have better evidence than the valuer had. Not louder opinions. Better evidence.Try another lender

Sometimes another lender reaches a different view. Sometimes they don't. Don't assume a second application fixes the underlying problem.

Other mistakes are avoidable. Don't rely on a portal estimate. Don't hide known issues such as previous subsidence, flood history or missing approvals for alterations. And don't instruct someone who knows “London” in the abstract but has no feel for the difference between, say, a period conversion in Stoke Newington and a 1930s semi in Beckenham.

Choosing a Surveyor and Preparing Your Property

The person carrying out the valuation matters almost as much as the property itself. You want someone qualified, independent and used to the sort of stock you own or are buying.

Who should carry out the valuation

For formal market valuations, RICS Chartered Surveyors must be registered under the RICS Valuers Registration Scheme, as set out in this overview of the RICS Valuers Registration Scheme requirement. That matters because the work has to be regulated, accountable and fit for purpose.

Independence matters too. If the valuer is tied to a lender, estate agent or developer, the role and brief may not align with what you need. If you need impartial advice, instruct an independent surveyor.

A sensible checklist looks like this:

- RICS status: check they are a RICS Chartered Surveyor

- Valuer registration: make sure they can undertake formal valuation work

- Relevant experience: period houses in Greenwich are not the same as dockside flats in Rotherhithe

- No conflicts: independence from the sale is important

- Clear scope: know exactly what report you're getting

If you want a practical checklist before instructing anyone, this guide on how to choose a building surveyor in London without wasting time or money is a sensible place to start.

Corinthian Surveyors London LTD is one example of an independent residential practice in this space. The firm is based in Forest Hill, covers London and the South East, and is run by Clive Thompson, who holds both RICS and CABE qualifications. It carries out market valuations, probate valuations, matrimonial separation valuations, capital gains tax valuations and survey work, with no ties to lenders, estate agents or developers.

How to prepare the property properly

You don't need to stage-manage the visit. You do need to make the inspection easy and give the valuer the facts.

Do these basic things:

- Provide access: open up lofts, cellars, garages and side returns

- Gather paperwork: planning permissions, building regulation certificates, warranties and lease documents if relevant

- List improvements: note what you've done and roughly when, without inflating the significance

- Be honest about defects: previous movement, flooding, roof repairs and neighbour disputes should not come as a surprise

- Tidy up: not because clutter changes value by magic, but because access and visibility matter

A proper valuation is an investment in certainty. It helps you price sensibly, negotiate from evidence and avoid expensive misunderstandings later.

FAQ

How much is my house worth in London

It depends on the exact location, property type, tenure, condition and recent sold comparables. In London, small differences in street, layout and repair can change value sharply, so an online estimate is only a rough starting point.

Is an estate agent valuation enough

It's enough if you only want a broad marketing opinion. It isn't enough for probate, tax, divorce, formal negotiations or any situation where the figure may be challenged.

Is a mortgage valuation the same as a survey

No. A mortgage valuation is for the lender's risk assessment. If you want advice on condition and defects, you need a survey such as a RICS Level 2 or Level 3 report.

What causes a down valuation in London

Usually one of three things. The agreed price is too high, the evidence from recent sales is weak or the property has risks such as defects, cladding issues, lease problems or flood exposure.

If you need a formal valuation or a survey on a residential property in London, Corinthian Surveyors London LTD handles market valuation, probate, matrimonial and related RICS work across the capital and surrounding areas. If you want to speak it through plainly before instructing, call 0800 00 16 422.