Property Valuation Reports in London: RICS Surveyors 2026

You've probably had this already. An estate agent gives you one figure. A lender gives you another. A solicitor asks for a formal valuation. Then someone mentions a survey, a Red Book report and lease length, and suddenly a simple flat in Brockley or a terrace in Bromley starts to feel far less simple.

Here's the straight answer. A proper valuation report is not a sales estimate and it isn't a box-ticking exercise. It's a formal opinion of value prepared for a defined purpose, and in London the details matter. Short leases, awkward titles, rights of way, poor EPC ratings, flood risk, unusual conversions and patchy condition all affect the final figure.

Table of Contents

- What Is a Property Valuation Report?

- The Different Types of Valuation Reports

- What a RICS Valuation Report Actually Contains

- Valuation Report vs Survey vs Mortgage Valuation

- When to Instruct a Chartered Surveyor for a Valuation

- The Corinthian Surveyors Valuation Process

- London Property Valuations FAQs and Red Flags

What Is a Property Valuation Report?

A property valuation report is a formal document that gives a surveyor's professional opinion of a property's value on a specific date, for a specific purpose. That purpose might be probate, divorce, tax, shared ownership staircasing, a sale, a purchase or a dispute between co-owners.

An estate agent's appraisal is different. It's often geared towards winning an instruction. That doesn't make it useless, but it does mean you shouldn't confuse it with a formal valuation that may need to stand up with HMRC, solicitors, a court or a lender.

Why the distinction matters

A proper valuation isn't a guess. It's based on inspection, market evidence, tenure, legal issues and the practical realities of the property. If I'm valuing a Victorian flat conversion in Peckham, I'm not just looking at the postcode and floor area. I'm looking at lease terms, repair obligations, condition, alterations, layout and how that property sits in the local market.

If you're dealing with a buy-to-let flat and wondering why the rent and the capital value don't always move in step, this piece on understanding rental property value disconnect is worth a read. It helps explain why a property can look strong on paper as an investment yet still attract a more cautious valuation figure.

Practical rule: If the figure needs to be defended to a third party, use a formal valuation report, not a free appraisal.

What gives it legal weight

A valuation report has standing because it is tied to a purpose and prepared under professional rules. The surveyor has to explain what has been valued, the basis of value and any assumptions that affect the figure.

That's especially important in London, where one clause in a lease or one unresolved title issue can change the result. A garden flat in Dulwich with a clean long lease is one thing. A similar flat in Lambeth with a short lease, escalating charges or restrictions on use is another.

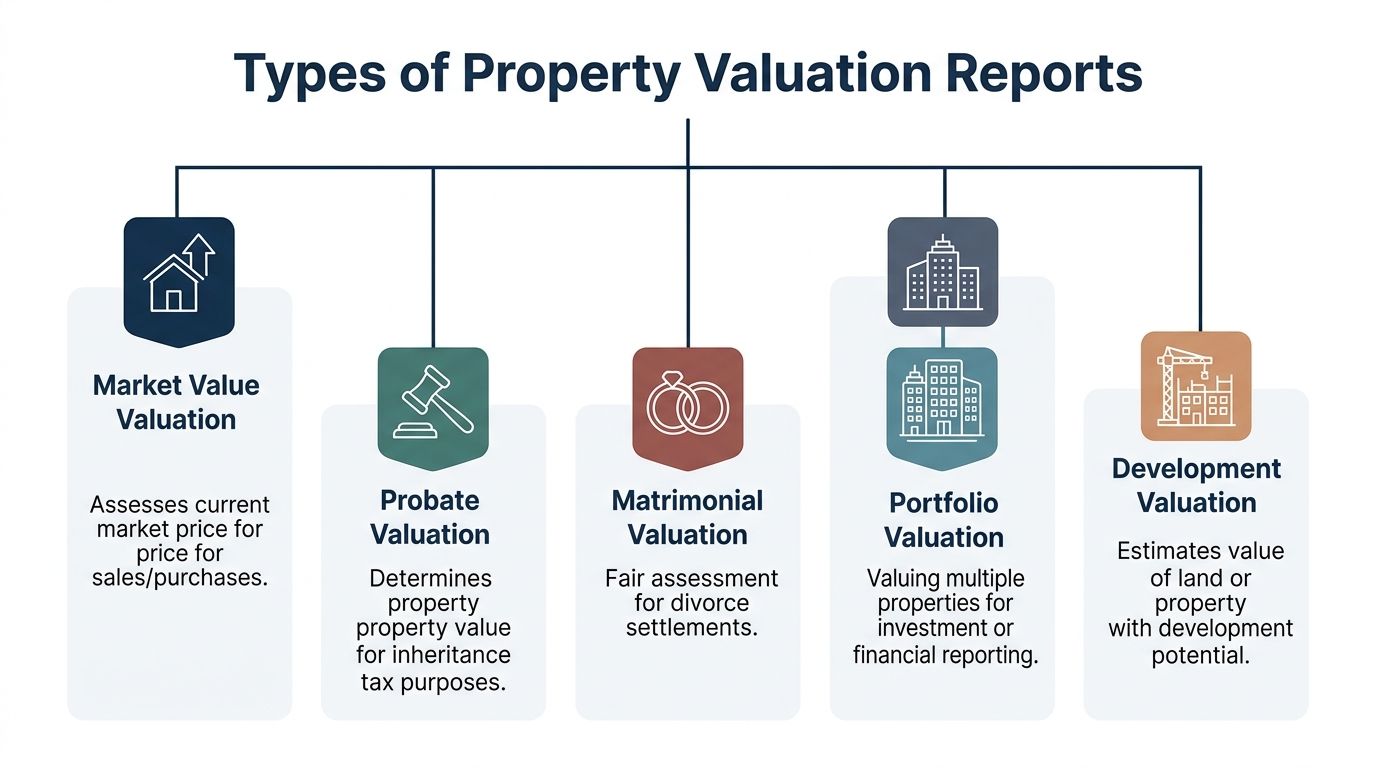

The Different Types of Valuation Reports

Not all property valuation reports are the same. The right report depends on what you need it for. Use the wrong one and you can waste time, create arguments and end up paying twice.

The main report types

Here's the plain-English version:

| Report type | Typical use | What matters most |

|---|---|---|

| Market valuation | Sale, purchase, transfer or general decision-making | Current market evidence and property condition |

| Probate valuation | Inheritance Tax and estate administration | Value at the relevant date and defensible reasoning |

| Matrimonial valuation | Divorce or separation proceedings | Independence and a fair figure both sides can rely on |

| Capital Gains Tax valuation | Tax reporting, often retrospective | Correct valuation date and supporting evidence |

| Shared ownership staircasing valuation | Buying further shares from a housing association | Compliance with the housing association's requirements |

A broader explanation of these is set out in property valuations in London and when you need one.

Probate, tax and legal work need precision

Probate and tax valuations are where people often come unstuck. The figure has to fit the legal purpose. It isn't enough to say what the property might have sold for “around that time”. The date matters. The market context matters. The property rights being valued matter.

A UK property valuation report must clearly state the property rights appraised, including encumbrances such as easements, restrictive covenants or rights-of-way, and identify the owner of record, in line with valuation guidance referenced here in the real estate valuation guidelines.

That sounds technical, but the effect is simple. If a house in Sydenham has a shared access issue, or a flat in Westminster has lease restrictions that limit use or value, the report has to deal with that.

London examples matter

In London, the same label can hide very different jobs.

- A market valuation in Bromley may hinge on condition, extension quality and how the house compares with nearby 1930s semis.

- A probate valuation in Islington may turn on date-specific evidence and whether the flat had a short lease at the relevant date.

- A matrimonial valuation in Greenwich must be independent and neutral. It can't be shaped to suit one side's position.

- A staircasing valuation in Woolwich needs to follow the housing association's rules and timescales.

A valuation only works if it matches the reason you need it. The purpose isn't paperwork. It drives the whole report.

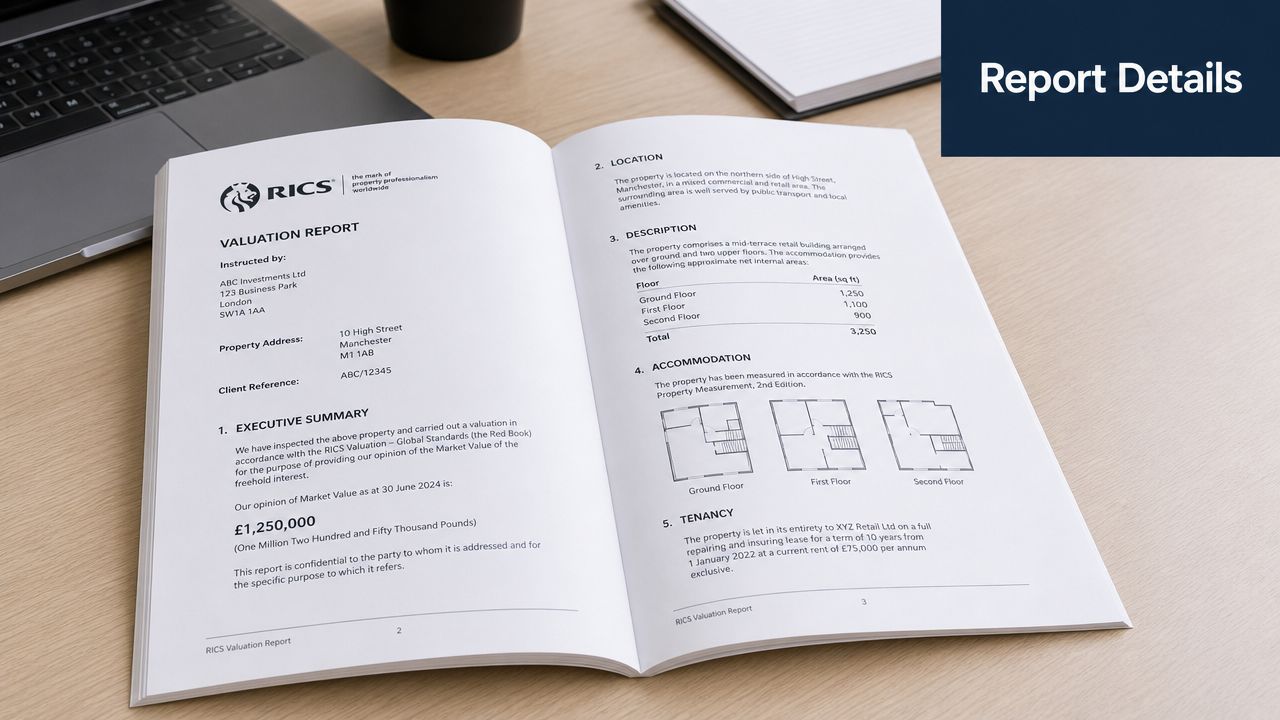

What a RICS Valuation Report Actually Contains

A proper RICS report should be readable. If it isn't, something has gone wrong. You should be able to see what was valued, why the figure was reached and what assumptions sit behind it.

The essentials you should expect

RICS Valuation Global Standards, known as the Red Book, require a valuation report giving an opinion of market value to state the date of value, the basis of value, the assumptions and special assumptions and to justify the valuation method used for the property type, as outlined in the RICS Red Book guidance summary.

In practice, that means your report should cover:

- The property itself: Address, type, accommodation, tenure and relevant physical features.

- The valuation date: This is important for probate, tax and any retrospective work.

- The basis of value: Open market value is common, but the report must say what basis has been used.

- Assumptions: For example, whether services are assumed to be operational or whether legal title is assumed to be good.

- Special assumptions: These apply where a scenario is being tested, such as altered lease terms.

- Method and evidence: Usually comparable market evidence for residential property, adjusted to reflect the subject property.

What the surveyor is actually analysing

The final number doesn't come from a spreadsheet alone. It comes from judgement applied to evidence.

A valuer will consider items such as:

- Tenure: Freehold, leasehold, share of freehold and the practical implications of each.

- Condition: Damp, cracking, roof defects, outdated kitchens, poor repair and unauthorised alterations.

- Location: Not just the borough, but the exact position, outlook, road, transport and market appeal.

- Legal baggage: Rights of way, covenants and anything else affecting value.

- Market tone: Comparable sales and how directly they relate to the property being valued.

If a report gives you a figure without making the assumptions clear, treat it with caution.

Why London reports need more detail

London property often has layers. A period conversion in Camberwell may have uneven maintenance history. A flat in Tower Hamlets may look strong until you inspect the lease terms. A house in a conservation area in Blackheath may have restrictions that matter to value and future works.

That's why a serious report doesn't just state the figure. It shows the route taken to get there.

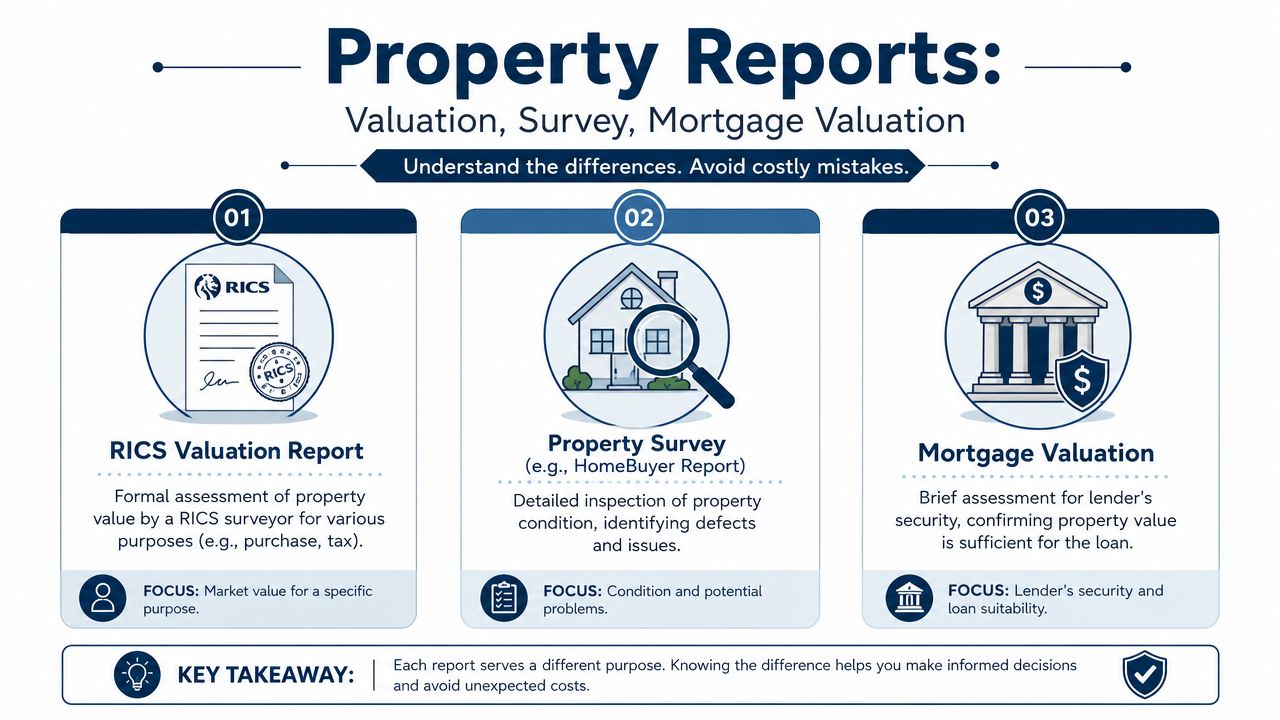

Valuation Report vs Survey vs Mortgage Valuation

Buyers often make expensive mistakes. A valuation report, a survey and a mortgage valuation are not the same thing. They serve different people and answer different questions.

The simple comparison

| Service | Who it is for | Main purpose | What it won't do |

|---|---|---|---|

| Valuation report | Client, solicitor, court, HMRC, lender in some cases | Gives a formal opinion of value | It won't replace a full condition survey |

| Survey | Buyer or owner | Examines condition and defects | It is not primarily a legal valuation document |

| Mortgage valuation | Lender | Checks the property is suitable security for the loan | It doesn't protect the buyer |

A clearer breakdown sits in this guide to what a RICS survey is.

Why mortgage valuations are limited

In the UK, use of Automated Valuation Models has grown substantially. A 2019 RICS report indicated that around 40 to 50% of mortgage valuations in the UK were being supported by AVMs or automated tools, although final lending decisions and detailed valuation reports still typically involved a chartered surveyor's oversight. For complex properties such as London leasehold flats or older buildings, human-led valuation reports remain the standard, as noted in this UK valuation overview.

That tells you two things. First, many lender valuations are quick and narrow in scope. Second, they are not a substitute for your own independent advice on condition.

A survey answers a different question

If you're buying a Victorian terrace in Lewisham, a Level 2 or Level 3 survey is where issues like damp, timber decay, roof spread, movement and poor alterations come to light. A valuation may reflect those issues if they are visible and value-relevant, but that isn't the same as a detailed building inspection.

Drainage is a good example. It can affect value, but it often needs separate investigation. If you want a plain explanation of what specialist drainage checks can reveal, Anytime Drain Solutions' survey insights are useful for homebuyers dealing with old pipework or suspected drainage defects.

Later in the process, this short explainer may help as well.

My blunt advice

Don't rely on the lender's valuation to tell you the property is sound. It won't. If you're buying in Southwark, Croydon or Wandsworth and the building is older, altered or converted, get the right survey as well as any valuation you need.

When to Instruct a Chartered Surveyor for a Valuation

Some situations leave no room for improvisation. If the figure will affect tax, a legal settlement or a transfer of money between parties, a proper valuation isn't optional.

The situations where you need one

You should instruct a chartered surveyor for a valuation when you are dealing with:

- Probate: The estate needs a defensible figure for the relevant date.

- Divorce or separation: Both parties need an independent opinion, not a sales pitch.

- Capital Gains Tax matters: The date and basis of value must fit the tax purpose.

- Shared ownership staircasing: Housing associations usually require a formal valuation.

- Transfer between family members or co-owners: A neutral figure helps avoid arguments.

- Sale or purchase decisions where accuracy matters: Especially where the property is unusual or disputed.

Why an estate agent's figure isn't enough

An estate agent can help you understand likely sale positioning. That's useful. But if a solicitor, HMRC or the court needs a valuation, they need a formal report with reasoning behind it.

That matters in real London scenarios. A flat in Clapham with a short lease can't be valued properly from photos and optimism. A probate house in Catford may have decades of deferred repair. A maisonette in Hackney may have title quirks that affect the figure. None of that is handled properly by a casual market appraisal.

One sensible check: before instructing anyone, read how to choose a building surveyor in London without wasting time or money. It will help you avoid panel-driven shortcuts and vague advice.

The cost of getting it wrong

The usual problem isn't that people get no figure at all. It's that they get the wrong type of figure from the wrong person, then try to use it for a job it was never meant to do.

That leads to delays, disputes and repeat work. If your solicitor has to go back and ask for a compliant report, you haven't saved anything.

The Corinthian Surveyors Valuation Process

You inherit a flat in Dulwich, the solicitor asks for a valuation, and within ten minutes you realise one detail could change the figure sharply. The lease has dropped, the EPC is poor, and the conversion paperwork looks thin. In London, that is normal. A proper valuation process has to catch those points early because they affect both the number and whether the report stands up under scrutiny.

The process starts with the brief. Give the surveyor the address, the reason for the valuation, and the exact date needed if the matter is probate, tax, divorce, or a retrospective dispute. If the property is leasehold, say so straight away. Lease length, ground rent terms, service charges, and any recent extension can alter the figure materially in London.

What happens from first call to report

At instruction stage, a competent valuer pins down the basis of value and the standard the report must meet. For RICS-regulated work, that means following Red Book requirements, not producing a loose opinion dressed up as a formal report. If a solicitor, court, lender, or tax adviser will rely on the valuation, the brief must be right before the inspection is booked.

The inspection comes next. The valuer measures the accommodation, checks condition, looks at layout, and records anything that affects marketability or value. In London this often includes alterations, evidence of movement, quality of conversion work, leasehold complications, EPC rating, and how the property sits within its exact micro-location. A basement flat on a busy road in Fulham is not judged the same way as a similar-sized flat on a better stretch two streets away.

Comparable evidence is then analysed against the property, not copied across lazily. This is where experience matters. London values turn on detail. A short lease in Kennington, a weak EPC in a rental-heavy block, or an absent freeholder in a Victorian conversion can all pull the final figure away from the headline prices clients see on portals.

Why independence matters

Use an independent valuer. You want a surveyor whose job is to give a defensible opinion, not support a sale pitch or keep a referrer happy.

Corinthian Surveyors London LTD is an independent RICS-regulated firm in Forest Hill run by Clive Thompson, who holds RICS and CABE qualifications. The firm undertakes residential valuation work across London, the Home Counties, and the South of England. That suits clients who need a clear report rather than sales talk. Buyers using a discreet London home search service often need the same thing. A valuation that is grounded in evidence and written to the right standard.

If the surveyor cannot explain the basis of value, the valuation date, and the assumptions in plain English, do not instruct them.

What you should receive

You should receive a written report that states the purpose, valuation date, basis of value, assumptions, and reasoning behind the figure. For London property, it should also show that the valuer has addressed the points that commonly distort value locally, especially lease terms, legal title issues, condition, alterations, and energy performance.

If you need to talk through the right report for a flat in Bermondsey, a house in Beckenham, or a probate property in Forest Hill, call 0800 00 16 422 before you instruct anyone. Getting the brief right at the start saves time, cost, and arguments later.

London Property Valuations FAQs and Red Flags

You agree a price for a flat in Hackney. A week later the valuation comes back lower. The reason is not guesswork or surveyor whim. In London, the figure often turns on points generic guides barely mention, such as a shortening lease, an awkward title, poor energy performance, or a sale nearby that looked comparable on a portal but was not comparable under Red Book scrutiny.

How does a short lease affect value

For London flats, a lease length below roughly 80 years can materially depress value, and how the surveyor derives that discount is a key part of an accurate RICS valuation report.

This is one of the biggest valuation traps in London. Two flats in the same block can look near-identical and still carry very different values because one has a healthy lease term and the other is drifting into marriage value territory. In boroughs such as Islington, Lambeth, Greenwich and Southwark, this comes up constantly. If the report glides over lease length, challenge it.

A proper valuation should deal with the unexpired term, ground rent, service charge position, and whether the market would price in the cost and hassle of a lease extension.

Do EPC ratings and climate issues affect the figure

Yes.

They affect buyer demand, lender appetite, and the likely cost of putting the property into a more acceptable condition. Under RICS Red Book rules, a valuer must reflect the market at the valuation date. If buyers are discounting draughty stock or lenders are cautious about properties with obvious efficiency problems, the valuation must reflect that.

In London, this is rarely abstract. A poor EPC on a Victorian terrace in Lewisham or a draughty conversion in Brixton may influence the figure where retrofit costs are obvious. The same applies where flooding, overheating, or hard-to-insure construction affects saleability.

What red flags should you look for in a report

Look for these warning signs:

- Unclear assumptions: The report should state what has been assumed about tenure, condition, alterations, planning, and legal matters.

- Weak comparable evidence: A valuation for a Battersea flat should rely on similar local sales, not convenient picks from a different micro-market.

- Vague lease analysis: If the lease term, rent review clauses, or extension position are brushed aside, the figure may be wrong.

- No adjustment reasoning: You should be able to see why the valuer placed the property above or below the comparables.

- Poor treatment of unusual stock: Listed buildings, converted houses, ex-local authority flats, and heavily altered homes need careful judgement.

- No clear Red Book basis: If the purpose, valuation date, and basis of value are muddy, the report is not doing its job.

Read the report like a client with money at stake, because that is exactly what you are.

Can you challenge a valuation

Yes, if you have evidence.

Good challenges are built on better comparables, corrected lease details, title information the valuer did not have, or clear condition points that were missed. Bad challenges are built on asking price screenshots and agent optimism. Those do not carry much weight.

If you are buying at the top end and want a sense of how certain parts of the market are being presented to purchasers, a discreet London home search can help you see how rare stock is being positioned. Keep the distinction clear. Marketing can shape expectations, but it does not replace valuation evidence.

Check the valuation date, basis of value, assumptions, tenure details, and comparable evidence before you focus on the final number.

FAQ

Is a mortgage valuation enough for a buyer in London?

No. It is prepared for the lender's security position, not to advise you on condition, risk, or whether you are paying too much.

Do I need a survey as well as a valuation report?

Often, yes. A valuation tells you the likely figure at a given date. A survey tells you what may be wrong with the building and what it could cost to put right.

Are leasehold flats harder to value than freehold houses?

Usually, yes. Lease length, service charges, restrictions, cladding issues, and repair liabilities all affect the figure.

Can a valuation be retrospective for tax purposes?

Yes, if the instruction is framed properly and the report states the correct valuation date and basis.

If you need a formal valuation that is clear, independent and suitable for a London residential property, Corinthian Surveyors London LTD handles market valuations, probate valuations, matrimonial separation valuations, capital gains tax work and shared ownership cases across London and the South East. Start with the purpose of the report and the property address, and the brief can be set correctly from the outset.